FedEx Stock Drops as Margin Pressure Clouds Freight Spin-Off Outlook

FedEx stock dropped after investors focused on weaker margins in its core delivery business and the uncertainty created by the recent FedEx Freight spin-off. Although the company reported stronger quarterly results and issued a 2026 outlook, the market reaction showed that investors want clearer proof that the slimmed-down FedEx can protect profits, control costs and grow without its highly profitable trucking unit.

What Happened

FedEx shares slid after the company’s latest earnings update showed that costs were eating into margins at its main delivery operation. The stock reaction came even though FedEx reported stronger revenue and profit than analysts expected, highlighting a key concern on Wall Street: investors are no longer looking only at headline growth. They are looking at whether FedEx can generate stronger profits after separating from FedEx Freight.

The company completed the spin-off of FedEx Freight on June 1, 2026, turning the trucking business into a separate publicly traded company. That move was designed to sharpen FedEx’s focus on its delivery network, but it also removed a business that had been viewed as one of the company’s more profitable segments. As a result, the market is now recalibrating how to value FedEx as a more focused package delivery company.

The immediate pressure came from the Federal Express segment, where operating margin fell to 7.7% from 8.4% a year earlier. FedEx said costs increased in areas such as employee salaries and benefits, outsourced transportation and fuel. For investors, that raised a difficult question: if the company is becoming more focused, can it also become more efficient fast enough?

The sell-off also reflected uncertainty around FedEx’s new calendar-year reporting system. The company is shifting away from its previous fiscal year ending in May, which makes near-term comparisons harder for analysts and investors. In simple terms, the numbers are not yet easy to compare with past models, and that creates more room for caution.

Key Details

FedEx forecast calendar 2026 adjusted earnings per share between $16.90 and $18.10. That guidance now reflects a company focused mainly on delivery operations, excluding the separated FedEx Freight business. While the forecast gives investors a new benchmark, analysts still need time to rebuild models around the new structure.

The logistics industry is also facing external pressure. FedEx and UPS have been dealing with weaker shipping volumes tied to changing U.S. trade policies. Higher fuel prices have added another challenge, especially for companies that operate large aircraft, truck and delivery networks. These cost pressures can quickly affect margins, even when revenue remains strong.

Another issue is the end of duty-free “de minimis” treatment for some low-value e-commerce shipments linked to China-based discount sellers such as Shein and Temu. That change has weighed on shipping volumes, because fewer low-cost packages may move through the same channels that previously benefited from the exemption.

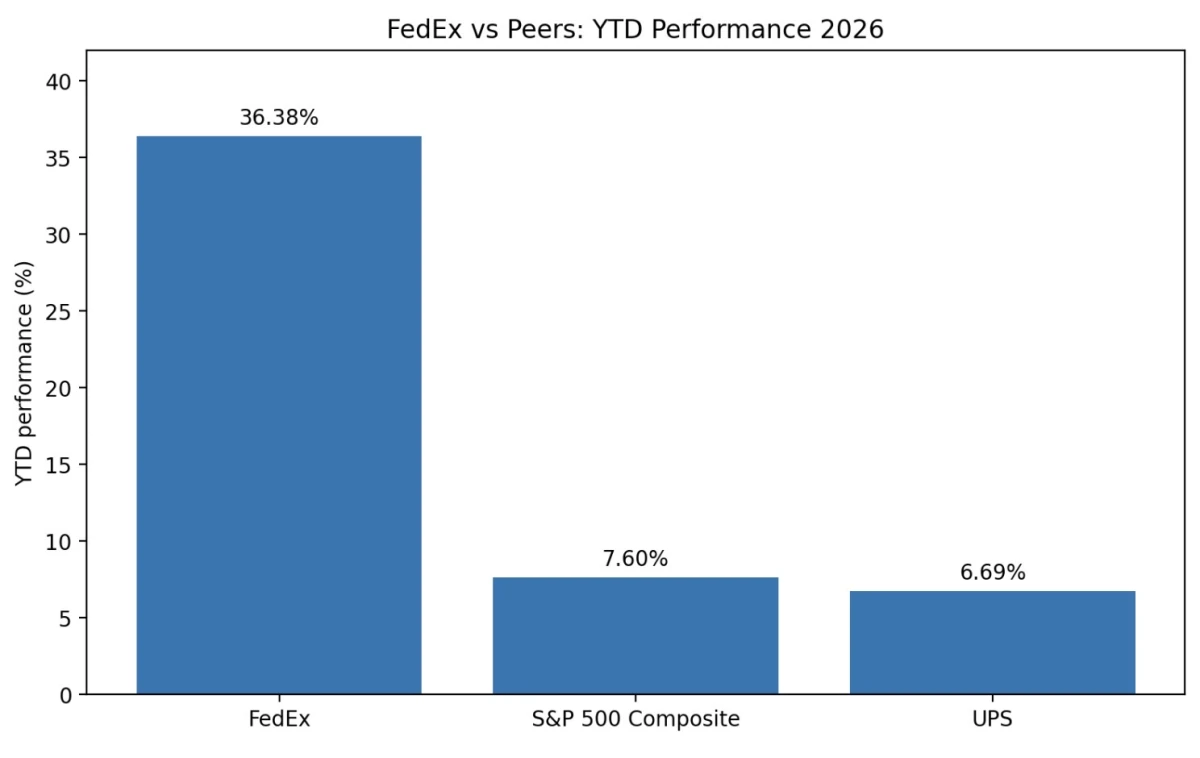

The chart provided shows that FedEx has still outperformed UPS and the S&P 500 Composite so far in 2026. FedEx was up 36.38% year to date, compared with 7.6% for the S&P 500 Composite and 6.69% for UPS. That outperformance helps explain why the stock was vulnerable to a sharper pullback: after a strong run, investors may react quickly when profit margins show weakness.

What Was Said

“It will be difficult to judge numbers for a few quarters given the noise.”

That view, attributed to Morgan Stanley analysts, captures the main challenge for investors. FedEx is not only reporting earnings; it is also changing its structure, changing its reporting calendar and operating in a tougher logistics market. That combination makes it harder to separate short-term accounting noise from the company’s underlying performance.

J.P. Morgan analysts also warned that FedEx could face an overhang while the market works through the moving pieces of the Freight spin-off and the shift to a calendar-year reporting period. In other words, the company may need several quarters to convince investors that the new structure can deliver stronger and more predictable profitability.

Why It Matters

FedEx matters because it is often seen as a bellwether for global trade. When FedEx reports pressure in package volumes, transportation costs or fuel expenses, investors often read those signals as clues about broader economic activity. A weaker margin profile can suggest that demand, pricing power or cost control is under pressure across the logistics sector.

The spin-off also matters because it changes how investors evaluate FedEx. Before the separation, FedEx Freight gave the company exposure to the less-than-truckload trucking market, a business with different economics from parcel delivery. Now, FedEx must prove that its core delivery network can stand on its own and still deliver attractive margins.

For customers, the issue is less about the stock price and more about service strategy. FedEx is likely to keep focusing on efficiency, route optimization, premium delivery services and higher-value business segments. If the company succeeds, it could become more focused and competitive. If costs keep rising faster than productivity gains, margin pressure could remain a concern.

For investors, the key debate is whether the FedEx Freight spin-off unlocks value or removes a stabilizing profit engine. Supporters may argue that a simpler FedEx can move faster and allocate capital more efficiently. Skeptics may argue that the company now has less margin support at a time when parcel delivery faces fuel, labor and volume headwinds.

What Happens Next

The next few quarters will be critical. Investors will watch whether FedEx can improve margins in its Federal Express segment and whether cost-saving initiatives can offset higher salaries, benefits, transportation expenses and fuel costs. The company’s ability to maintain pricing power will also be important, especially if shipping volumes remain uneven.

Analysts will also need time to compare FedEx’s new calendar-year outlook with the company’s previous structure. Because the forecast now reflects the post-spin-off delivery business, direct comparisons with past results are more complicated. That means management commentary, operating margin trends and cash flow guidance may carry more weight than usual.

FedEx Freight will also remain part of the investor conversation, even as a separate company. Its performance may influence how markets judge whether the separation created value. If both companies execute well, the spin-off could be seen as a successful restructuring. If either business struggles, investors may question whether the timing was ideal.

The broader logistics backdrop will be just as important. Fuel prices, trade policy, e-commerce shipment rules and industrial demand can all affect FedEx and UPS. A recovery in volumes would help. Continued cost inflation would make the path more difficult.

Key Facts

- FedEx shares fell after investors focused on margin pressure in its core delivery segment.

- The Federal Express segment operating margin declined to 7.7% from 8.4% a year earlier.

- FedEx completed the spin-off of FedEx Freight on June 1, 2026.

- The company forecast calendar 2026 adjusted earnings of $16.90 to $18.10 per share.

- FedEx has outperformed UPS and the S&P 500 Composite year to date, according to the provided chart data.

Conclusion

FedEx stock dropped because investors are looking beyond revenue growth and focusing on whether the company can protect margins after the FedEx Freight spin-off. The next test will be execution: FedEx must show that a more focused delivery business can improve efficiency, manage costs and grow earnings under its new calendar-year structure. For now, the market is waiting for clearer evidence that the slimmer FedEx can turn its restructuring into stronger long-term profitability.

Frequently Asked Questions

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

Comments (0)